Pay for Long Term Care

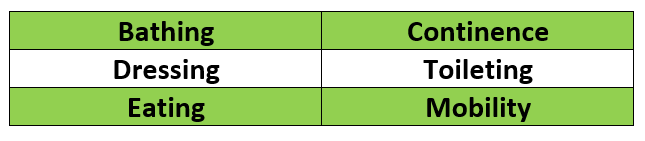

- Buy a long-term care insurance policy– these policies are designed to cover all or a decent portion of the costs related to long term care event, or situation. The policies are triggered when the insured person cannot perform 2 of 6 “activities of daily living” for either physical or cognitive reasons.

The 6 Activities of Daily Living

These long-term care insurance policies are effective in addressing this problem, but may be hard to buy, unless you are in good health, with no chronic conditions. They can also be expensive, depending upon your age, and the level of benefits you desire. Additionally, the premiums will increase over time, sometimes significantly. Finally, if you die peacefully in your sleep, having never needed to use the policy for long-term care expenses, the company does not give back any of the premiums you paid, even if you paid them for 25-35 years or more.

4. Buy a Life Insurance Retirement Plan (LIRP)- a LIRP is a newer type of life insurance policy that offers “living benefits” in the form of tax-free income opportunities, and a chronic illness rider that can provide a large pool of tax-free money for long term care needs.

4. Buy a Life Insurance Retirement Plan (LIRP)- a LIRP is a newer type of life insurance policy that offers “living benefits” in the form of tax-free income opportunities, and a chronic illness rider that can provide a large pool of tax-free money for long term care needs.

The chronic illness rider is triggered when the insured cannot perform 2 of 6 activities of daily living, as with the more traditional long-term care insurance policies. The benefit comes in the form of an acceleration of the death benefit, which is received tax-free over a period of years. If the chronic illness rider is never used or needed, the policy beneficiaries will receive the death benefit on a tax-free basis.

So LIRPs are a more efficient way to address the long-term care risk, because you typically only pay premiums for 5-10 years, and all of the money (and then some) you pay in, stays in the family- either through use of the long-term care/chronic illness rider, or through the receipt of the tax-free death benefit by the beneficiaries. Also, the under-writing process for LIRPs is generally easier than it is for long-term care policies.

5. Buy an asset based LTC plan- asset based long-term care plans allow you to use “rainy day” funds, or lower yielding assets you do not need for income, for the purpose of long-term care. It allows you to leverage a given amount of money into a much larger tax-free long-term care benefit (if needed) generally with only a one-time payment. If you never need the care, a tax-free death benefit (these plans use a whole life policy for the LTC, but do not offer opportunities for tax-free income or the flexibility of the LIRP discussed in #4 above), goes to your loved ones. You can use low yielding savings, or retirement account assets, or even home equity for these leveraged tax-free plans.

The objective of an extended care plan is not to protect assets alone…it is to protect income streams as well!

Our planning can create large pools of money, or significant new income streams to address the costs of the chronic illness or long-term care event. (It is actually not an event- it’s a condition)

As professionals who are Certified in Long Term Care, we also try to make clients aware of the fact that there are NON-FINANCIAL CONSEQUENCES when a long-term care event strikes, as well as the more obvious financial ones.