Get in touch

631-592-1423

83 South St, Freehold, NJ 07728, United States of America

The 5 Ways to Plan or Pay for Long Term Care

1) Do nothing

If you do no planning at all, you are essentially saying, well, if it happens, I will use my savings to pay for it, I will self-insure. For those single or married people who have a lot of assets, this can be a viable plan. Also, for those people for whom leaving a legacy behind is not at all important, this may be a viable way to go.

For other people, this is not a viable route for three main reasons:

- There is a real chance of running out of money- after which you would be subject to relying on public assistance (“Medicaid”) for all your daily needs.

- The Medicare “spend down” rules require a married couple to use most of their marital assets to address the expenses of the impaired spouse. The healthier, or community spouse (still living in the community on their own) may be accidentally impoverished and have a more precarious retirement than originally thought if there is no planning for these circumstances. For example, the Community Spouse Resource Allowance, as of 2022, is approximately $130,400. A house and a car, and potentially a couple of other assets, plus about 2500-3000/month of income, are also allowable or exempt from the Medicaid spend down rules.

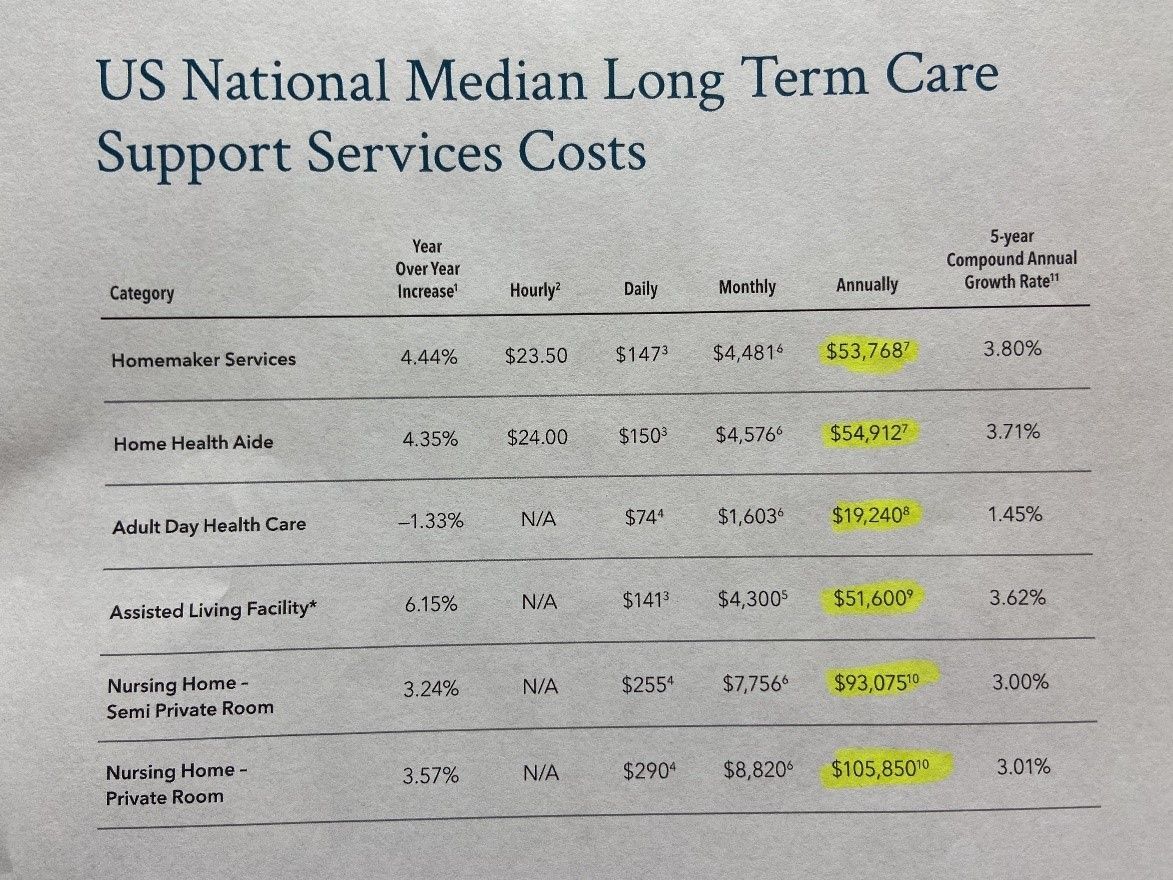

- Since the statistical odds of needing long term care before we die are so high (about a 70% chance, according to the US Department of Health and Humans Services- see sidebar), and because this type of care is so expensive, without proper planning, you can accidentally destroy the legacy you were planning to leave to loved ones.

4) Buy a Long-term Care Insurance Policy

These policies are designed to cover all or a decent portion of the costs related to long term care event, or situation. The policies are triggered when the insured person cannot perform 2 of 6 “activities of daily living” for either physical or cognitive reasons.

The 6 Activities of Daily Living

- Bathing

- Dressing

- Eating

- Continence

- Toileting

- Mobility

These long-term care insurance policies are effective in addressing this problem, but may be hard to buy, unless you are in good health, with no chronic conditions. They can also be expensive, depending upon your age, and the level of benefits you desire. Additionally, the premiums will increase over time, sometimes significantly.

Finally, if you die peacefully in your sleep, having never needed to use the policy for long-term care expenses, the company does not give back any of the premiums you paid, even if you paid them for 25-35 years or more.

5) Buy an Asset Based LTC Plan

Asset based long-term care plans allow you to use “rainy day” funds, or lower yielding assets you do not need for income, for the purpose of long-term care. It allows you to leverage a given amount of money into a much larger tax-free long-term care benefit (if needed) generally with only a one-time payment. If you never need the care, a tax-free death benefit (these plans use a whole life policy for the LTC, but do not offer opportunities for tax-free income or the flexibility of the LIRP discussed in #4 above), goes to your loved ones. You can use low yielding savings, or retirement account assets, or even home equity for these leveraged tax-free plans.

The objective of an extended care plan is not to protect assets alone…it is to protect income streams as well!

Our planning can create large pools of money, or significant new income streams to address the costs of the chronic illness or long-term care event. (It is actually not an event- it’s a condition)

As professionals who are Certified in Long Term Care, we also try to make clients aware of the fact that there are NON-FINANCIAL CONSEQUENCES when a long-term care event strikes, as well as the more obvious financial ones.

Contact Us Today!

Protect your assets and ensure your peace of mind for long-term care—call us now for expert guidance.

908-325-0335

83 South St, Freehold, NJ 07728, United States of America

Services

Sitemap

©2024 All Rights Reserved | Privacy Policy